import pandas as pd

import numpy as np

from matplotlib import pyplot as plt

import seaborn as sns

import matplotlib

from cycler import cycler

color = ["0.0", "0.4", "0.8"]

default_cycler = cycler(color=color)

linestyle = ["-", "--", ":", "-."]

marker = ["o", "v", "d", "p"]

plt.rc("axes", prop_cycle=default_cycler)

matplotlib.rcParams.update({"font.size": 18})6장 - 이질적 처치효과

6.1 ATE에서 CATE로

Why Prediction is not the Answer

CATE with Regression

data = pd.read_csv("../data/daily_restaurant_sales.csv")

data.head()| rest_id | day | month | weekday | weekend | is_holiday | is_dec | is_nov | competitors_price | discounts | sales | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | 2016-01-01 | 1 | 4 | False | True | False | False | 2.88 | 0 | 79.0 |

| 1 | 0 | 2016-01-02 | 1 | 5 | True | False | False | False | 2.64 | 0 | 57.0 |

| 2 | 0 | 2016-01-03 | 1 | 6 | True | False | False | False | 2.08 | 5 | 294.0 |

| 3 | 0 | 2016-01-04 | 1 | 0 | False | False | False | False | 3.37 | 15 | 676.5 |

| 4 | 0 | 2016-01-05 | 1 | 1 | False | False | False | False | 3.79 | 0 | 66.0 |

import statsmodels.formula.api as smf

X = ["C(month)", "C(weekday)", "is_holiday", "competitors_price"]

regr_cate = smf.ols(f"sales ~ discounts*({'+'.join(X)})", data=data).fit()ols_cate_pred = regr_cate.predict(

data.assign(discounts=data["discounts"] + 1)

) - regr_cate.predict(data)Evaluating CATE Predictions

train = data.query("day<'2018-01-01'")

test = data.query("day>='2018-01-01'")X = ["C(month)", "C(weekday)", "is_holiday", "competitors_price"]

regr_model = smf.ols(f"sales ~ discounts*({'+'.join(X)})", data=train).fit()

cate_pred = regr_model.predict(

test.assign(discounts=test["discounts"] + 1)

) - regr_model.predict(test)from sklearn.ensemble import GradientBoostingRegressor

X = ["month", "weekday", "is_holiday", "competitors_price", "discounts"]

y = "sales"

np.random.seed(42)

ml_model = GradientBoostingRegressor(n_estimators=50).fit(train[X], train[y])

ml_pred = ml_model.predict(test[X])np.random.seed(123)

test_pred = test.assign(

ml_pred=ml_pred,

cate_pred=cate_pred,

rand_m_pred=np.random.uniform(-1, 1, len(test)),

)test_pred[["rest_id", "day", "sales", "ml_pred", "cate_pred", "rand_m_pred"]].head()| rest_id | day | sales | ml_pred | cate_pred | rand_m_pred | |

|---|---|---|---|---|---|---|

| 731 | 0 | 2018-01-01 | 251.5 | 236.312960 | 41.355802 | 0.392938 |

| 732 | 0 | 2018-01-02 | 541.0 | 470.218050 | 44.743887 | -0.427721 |

| 733 | 0 | 2018-01-03 | 431.0 | 429.180652 | 39.783798 | -0.546297 |

| 734 | 0 | 2018-01-04 | 760.0 | 769.159322 | 40.770278 | 0.102630 |

| 735 | 0 | 2018-01-05 | 78.0 | 83.426070 | 40.666949 | 0.438938 |

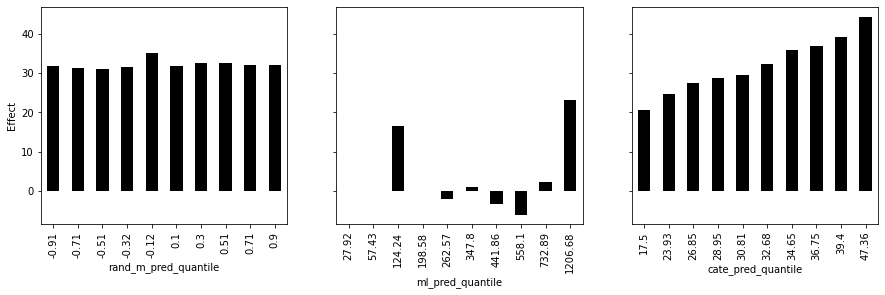

Effect by Model Quantile

from toolz import curry

@curry

def effect(data, y, t):

return np.sum((data[t] - data[t].mean()) * data[y]) / np.sum(

(data[t] - data[t].mean()) ** 2

)effect(test, "sales", "discounts")32.16196368039615def effect_by_quantile(df, pred, y, t, q=10):

# makes quantile partitions

groups = np.round(pd.IntervalIndex(pd.qcut(df[pred], q=q)).mid, 2)

return (

df.assign(**{f"{pred}_quantile": groups})

.groupby(f"{pred}_quantile")

# estimate the effect on each quantile

.apply(effect(y=y, t=t))

)

effect_by_quantile(test_pred, "cate_pred", y="sales", t="discounts")cate_pred_quantile

17.50 20.494153

23.93 24.782101

26.85 27.494156

28.95 28.833993

30.81 29.604257

32.68 32.216500

34.65 35.889459

36.75 36.846889

39.40 39.125449

47.36 44.272549

dtype: float64import warnings

warnings.filterwarnings("ignore")

fig, axs = plt.subplots(1, 3, sharey=True, figsize=(15, 4))

for m, ax in zip(["rand_m_pred", "ml_pred", "cate_pred"], axs):

effect_by_quantile(test_pred, m, "sales", "discounts").plot.bar(ax=ax)

ax.set_ylabel("Effect")

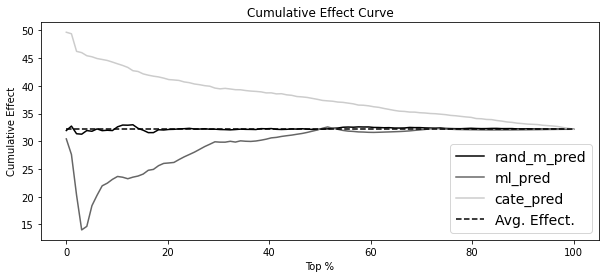

Cumulative Effect

np.set_printoptions(linewidth=80, threshold=10)def cumulative_effect_curve(dataset, prediction, y, t, ascending=False, steps=100):

size = len(dataset)

ordered_df = dataset.sort_values(prediction, ascending=ascending).reset_index(

drop=True

)

steps = np.linspace(size / steps, size, steps).round(0)

return np.array(

[effect(ordered_df.query(f"index<={row}"), t=t, y=y) for row in steps]

)

cumulative_effect_curve(test_pred, "cate_pred", "sales", "discounts")array([49.65116279, 49.37712454, 46.20360341, ..., 32.46981935, 32.33428884,

32.16196368])plt.figure(figsize=(10, 4))

for m in ["rand_m_pred", "ml_pred", "cate_pred"]:

cumu_effect = cumulative_effect_curve(test_pred, m, "sales", "discounts", steps=100)

x = np.array(range(len(cumu_effect)))

plt.plot(100 * (x / x.max()), cumu_effect, label=m)

plt.hlines(

effect(test_pred, "sales", "discounts"),

0,

100,

linestyles="--",

color="black",

label="Avg. Effect.",

)

plt.xlabel("Top %")

plt.ylabel("Cumulative Effect")

plt.title("Cumulative Effect Curve")

plt.legend(fontsize=14)

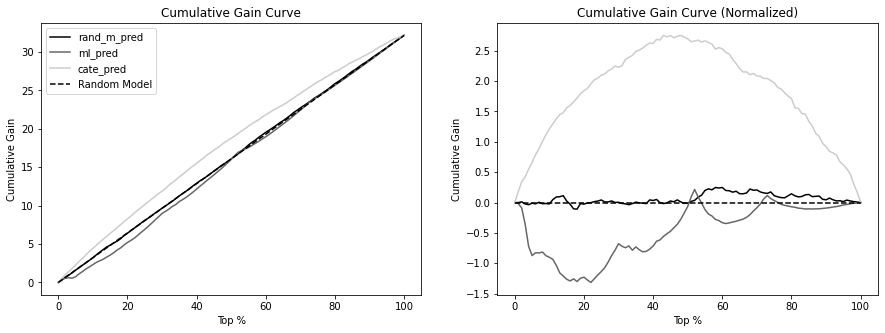

Cumulative Gain

def cumulative_gain_curve(

df, prediction, y, t, ascending=False, normalize=False, steps=100

):

effect_fn = effect(t=t, y=y)

normalizer = effect_fn(df) if normalize else 0

size = len(df)

ordered_df = df.sort_values(prediction, ascending=ascending).reset_index(drop=True)

steps = np.linspace(size / steps, size, steps).round(0)

effects = [

(effect_fn(ordered_df.query(f"index<={row}")) - normalizer) * (row / size)

for row in steps

]

return np.array([0] + effects)

cumulative_gain_curve(test_pred, "cate_pred", "sales", "discounts")array([ 0. , 0.50387597, 0.982917 , ..., 31.82346463, 32.00615008,

32.16196368])fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(15, 5))

for m in ["rand_m_pred", "ml_pred", "cate_pred"]:

cumu_gain = cumulative_gain_curve(test_pred, m, "sales", "discounts")

x = np.array(range(len(cumu_gain)))

ax1.plot(100 * (x / x.max()), cumu_gain, label=m)

ax1.plot(

[0, 100],

[0, effect(test_pred, "sales", "discounts")],

linestyle="--",

label="Random Model",

color="black",

)

ax1.set_xlabel("Top %")

ax1.set_ylabel("Cumulative Gain")

ax1.set_title("Cumulative Gain Curve")

ax1.legend()

for m in ["rand_m_pred", "ml_pred", "cate_pred"]:

cumu_gain = cumulative_gain_curve(

test_pred, m, "sales", "discounts", normalize=True

)

x = np.array(range(len(cumu_gain)))

ax2.plot(100 * (x / x.max()), cumu_gain, label=m)

ax2.hlines(0, 0, 100, linestyle="--", label="Random Model", color="black")

ax2.set_xlabel("Top %")

ax2.set_ylabel("Cumulative Gain")

ax2.set_title("Cumulative Gain Curve (Normalized)")Text(0.5, 1.0, 'Cumulative Gain Curve (Normalized)')

for m in ["rand_m_pred", "ml_pred", "cate_pred"]:

gain = cumulative_gain_curve(test_pred, m, "sales", "discounts", normalize=True)

print(f"AUC for {m}:", sum(gain))AUC for rand_m_pred: 6.0745233598544495

AUC for ml_pred: -45.44063124684

AUC for cate_pred: 181.74573239200615Target Transformation

X = ["C(month)", "C(weekday)", "is_holiday", "competitors_price"]

y_res = smf.ols(f"sales ~ {'+'.join(X)}", data=test).fit().resid

t_res = smf.ols(f"discounts ~ {'+'.join(X)}", data=test).fit().resid

tau_hat = y_res / t_resfrom sklearn.metrics import mean_squared_error

for m in ["rand_m_pred", "ml_pred", "cate_pred"]:

wmse = mean_squared_error(tau_hat, test_pred[m], sample_weight=t_res**2)

print(f"MSE for {m}:", wmse)MSE for rand_m_pred: 1115.803515760459

MSE for ml_pred: 576256.7425385397

MSE for cate_pred: 42.90447405550281When Prediction Models are Good for Effect Ordering

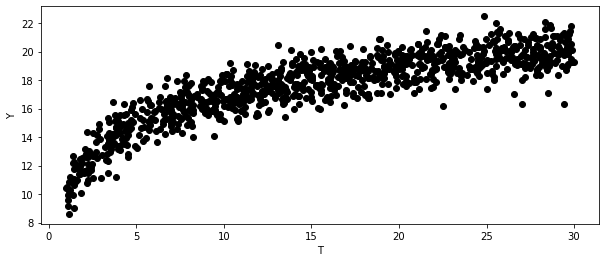

Marginal Decreasing Returns

np.random.seed(123)

n = 1000

t = np.random.uniform(1, 30, size=n)

y = np.random.normal(10 + 3 * np.log(t), size=n)

plt.figure(figsize=(10, 4))

plt.scatter(t, y)

plt.ylabel("Y")

plt.xlabel("T")Text(0.5, 0, 'T')

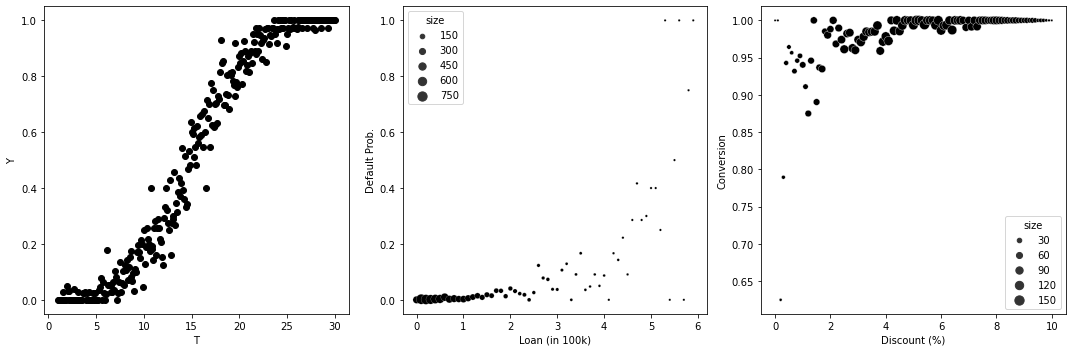

Binary Outcomes

np.random.seed(123)

fig, (ax1, ax2, ax3) = plt.subplots(1, 3, figsize=(15, 5))

n = 10000

t = np.random.uniform(1, 30, size=n).round(1)

y = (np.random.normal(t, 5, size=n) > 15).astype(int)

df_sim = pd.DataFrame(dict(t=t, y=y)).groupby("t")["y"].mean().reset_index()

df_sim

ax1.scatter(df_sim["t"], df_sim["y"])

ax1.set_ylabel("Y")

ax1.set_xlabel("T")

n = 10000

t = np.random.exponential(1, n).round(1).clip(0, 8)

y = (np.random.normal(t, 2, size=n) > 6).astype(int)

df_sim = (

pd.DataFrame(dict(t=t, y=y, size=1))

.query("t<6")

.groupby("t")

.agg({"y": "mean", "size": "sum"})

.reset_index()

)

sns.scatterplot(data=df_sim, y="y", x="t", size="size", ax=ax2, sizes=(5, 100))

ax2.set_ylabel("Default Prob.")

ax2.set_xlabel("Loan (in 100k)")

n = 10000

t = np.random.beta(2, 2, n).round(2) * 10

y = (np.random.normal(5 + t, 4, size=n) > 0).astype(int)

df_sim = (

pd.DataFrame(dict(t=t, y=y, size=1))

.groupby("t")

.agg({"y": "mean", "size": "sum"})

.reset_index()

)

sns.scatterplot(data=df_sim, y="y", x="t", size="size", ax=ax3, sizes=(5, 100))

ax3.set_ylabel("Conversion")

ax3.set_xlabel("Discount (%)")

plt.tight_layout()

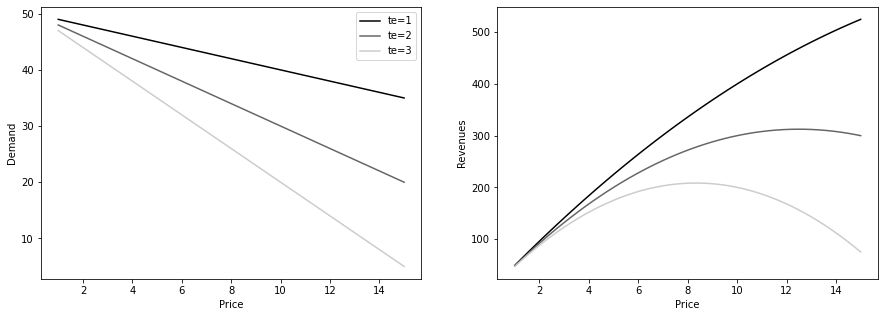

CATE for Decision Making

def demand(price, tau):

return 50 - tau * price

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(15, 5))

prices = np.linspace(1, 15)

for i, tau in enumerate([1, 2, 3]):

q = demand(prices, tau)

ax1.plot(prices, q, color=f"C{i}", label=f"te={tau}")

ax2.plot(prices, q * prices, color=f"C{i}", label=f"te={tau}")

ax1.set_ylabel("Demand")

ax1.set_xlabel("Price")

ax2.set_ylabel("Revenues")

ax2.set_xlabel("Price")

ax1.legend()

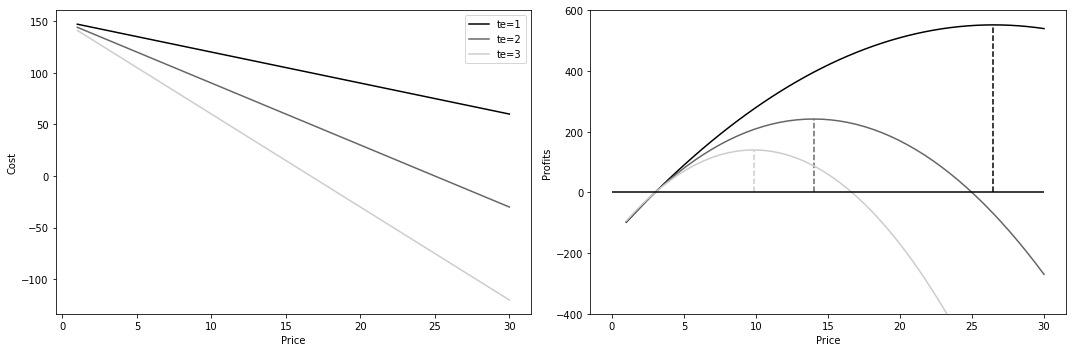

def cost(q):

return q * 3

def profit(price, tau):

q = demand(price, tau)

return q * price - cost(q)

prices = np.linspace(1, 30)

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(15, 5))

for i, tau in enumerate([1, 2, 3]):

profits = profit(prices, tau)

max_price = prices[np.argmax(profits)]

ax1.plot(prices, cost(demand(prices, tau)), label=f"te={tau}")

ax2.plot(prices, profits, color=f"C{i}", label=f"te={tau}")

ax2.vlines(max_price, 0, max(profits), color=f"C{i}", linestyle="--")

ax2.set_ylim(-400, 600)

ax2.hlines(0, 0, max(prices), color="black")

# ax2.legend()

ax2.set_ylabel("Profits")

ax2.set_xlabel("Price")

ax1.legend()

ax1.set_ylabel("Cost")

ax1.set_xlabel("Price")

plt.tight_layout()